DEFINING COMPETITION

WHAT IS PAVEMENT COMPETITION?

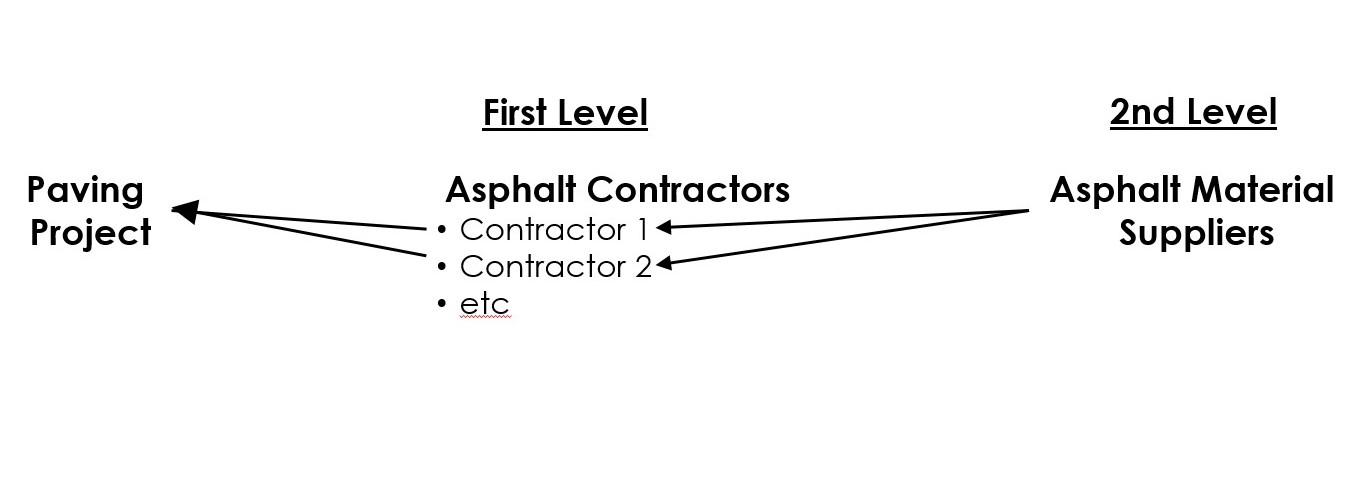

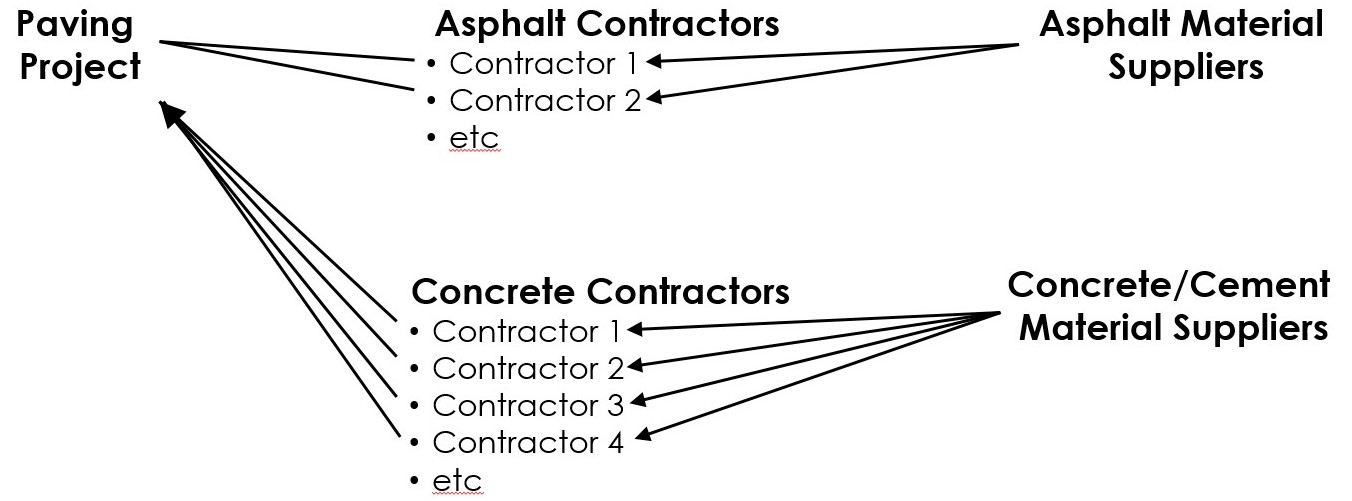

In the supply chain for pavement projects, there are two forms of competition:

INTRA-INDUSTRY COMPETITION

Intra-Industry (Contractor) Competition exists between firms that pave with the same material.

INTER-INDUSTRY COMPETITION

Inter-Industry (Material) Competition presents between firms that pave with (different) material substitutes.

When paving projects receive bids from contractors of only one material provider, competition is limited to just one level of the supply chain.

Inter-Industry Competition brings another level of competition to pavement letting.

ALABAMA’S HISTORY OF PAVEMENT COMPETITION

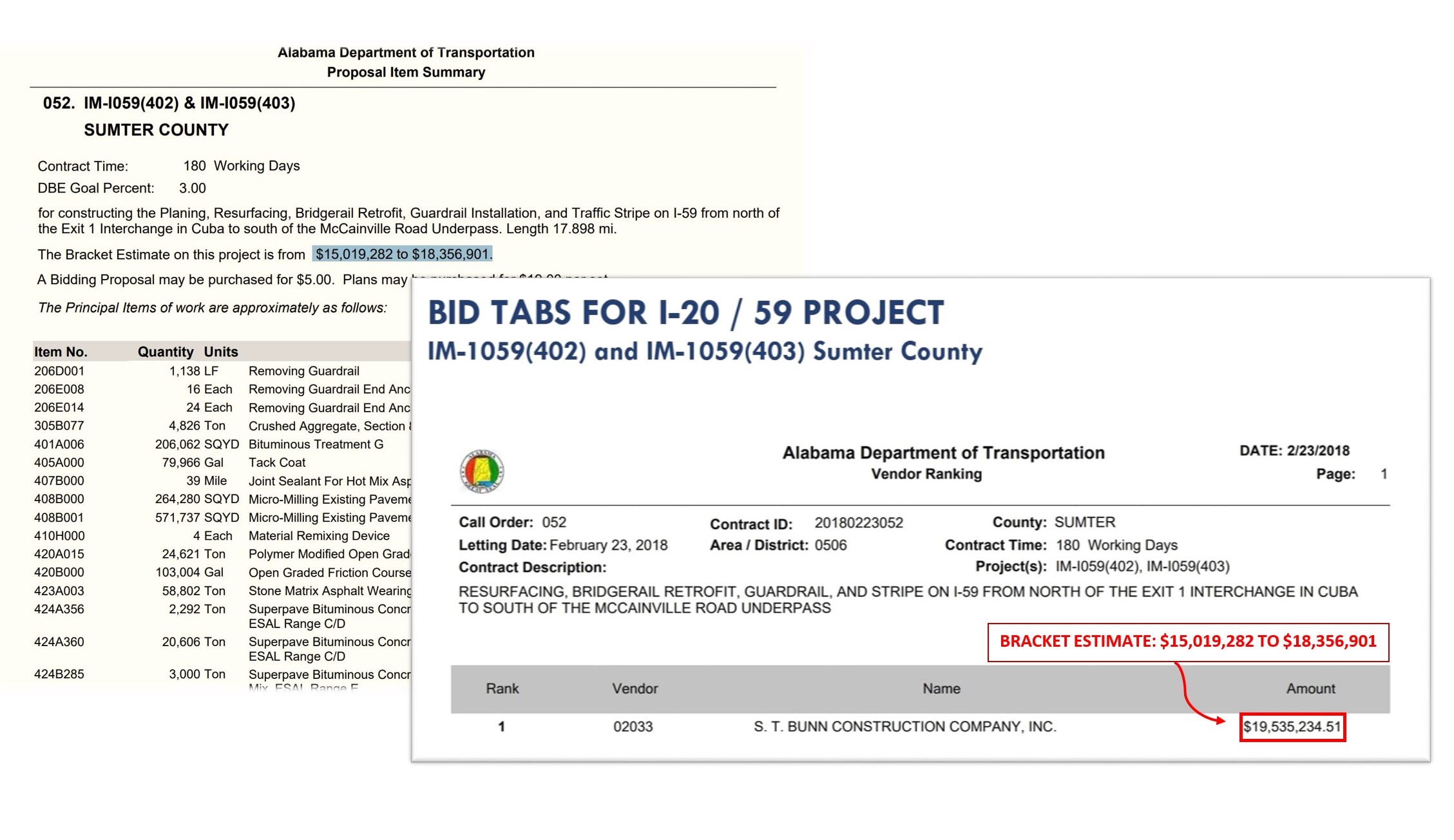

ZERO COMPETITION

ALDOT Bid Tabs for the February 23, 2018 I-59 Asphalt Resurfacing Project display how letting with zero competition in bids, the project is often awarded above the highest end of Bracket Estimate.

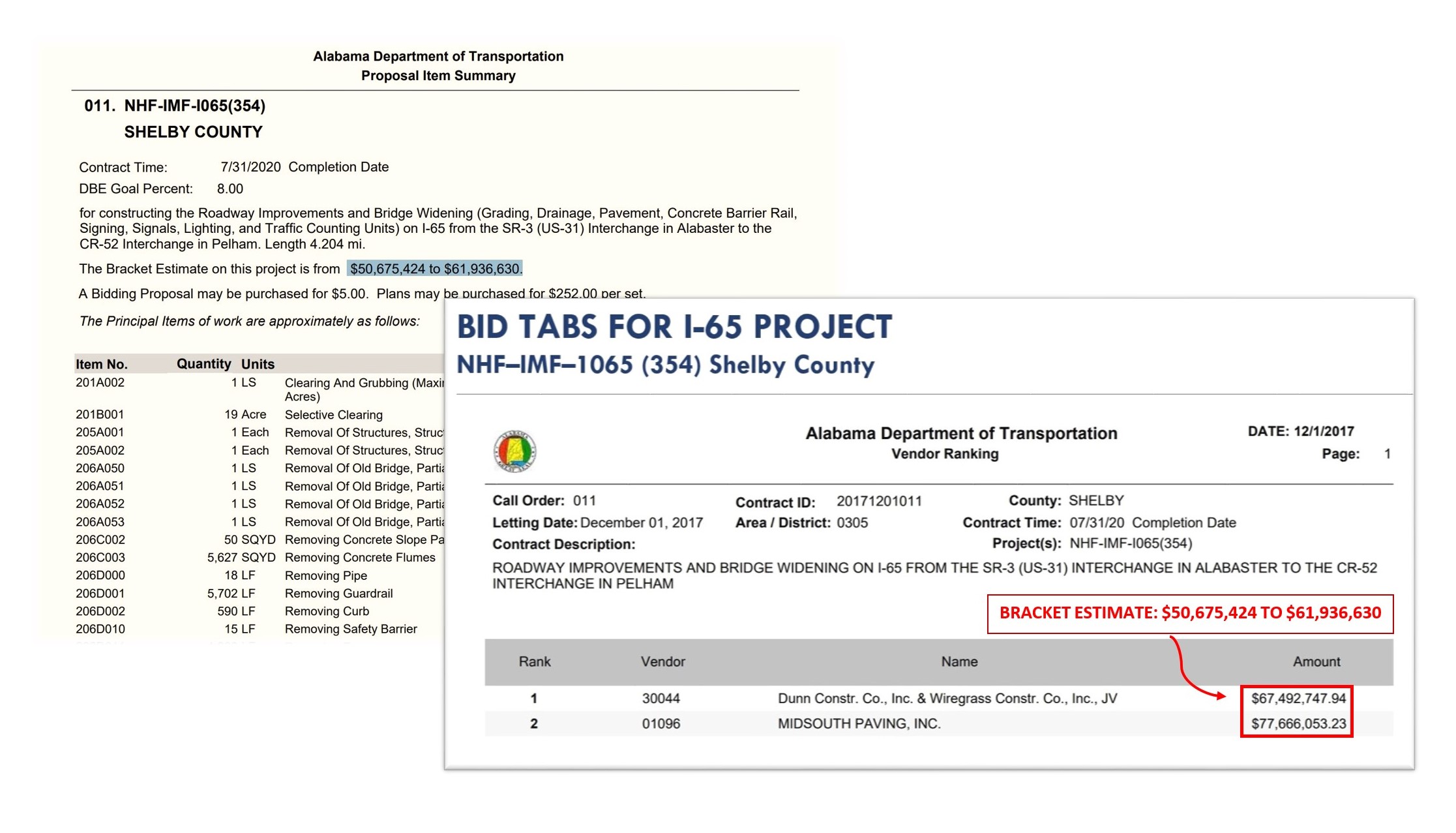

LIMITED COMPETITION

The December 1, 2017 I-65 Asphalt Roadway Improvements & Bridge Widening Project, a joint bid was allowed, thus limiting competition and resulting in both bids and award above the highest end of the Bracket Estimate.

MODERATE COMPETITION

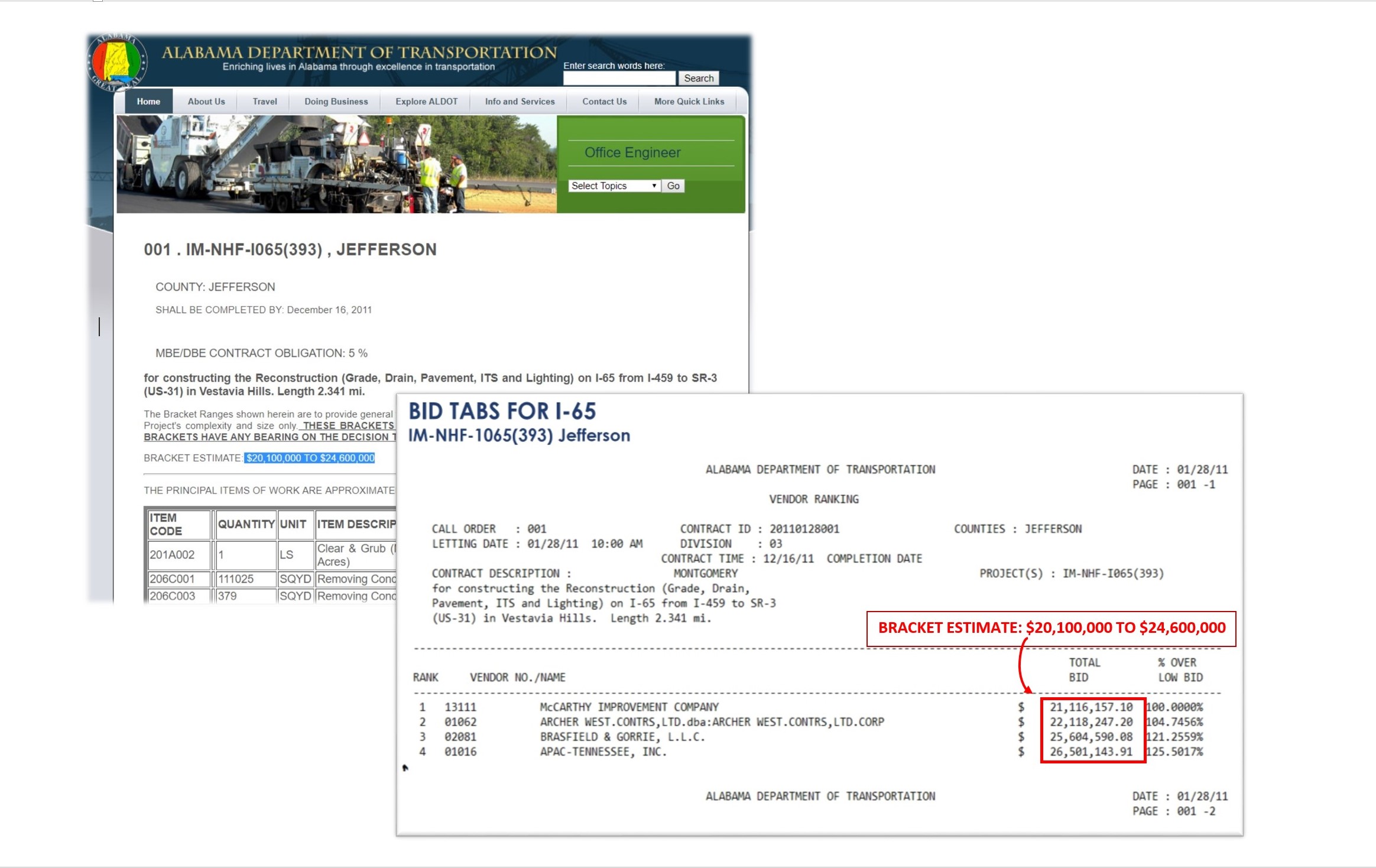

Alternatively, ALDOT Bid Tabs for an I-65 Concrete Reconstruction Project (January 28, 2011) show that moderate (4) vendor competition leads to multiple bids falling well within the Bracket Estimate.

SUBSTANTIAL COMPETITION

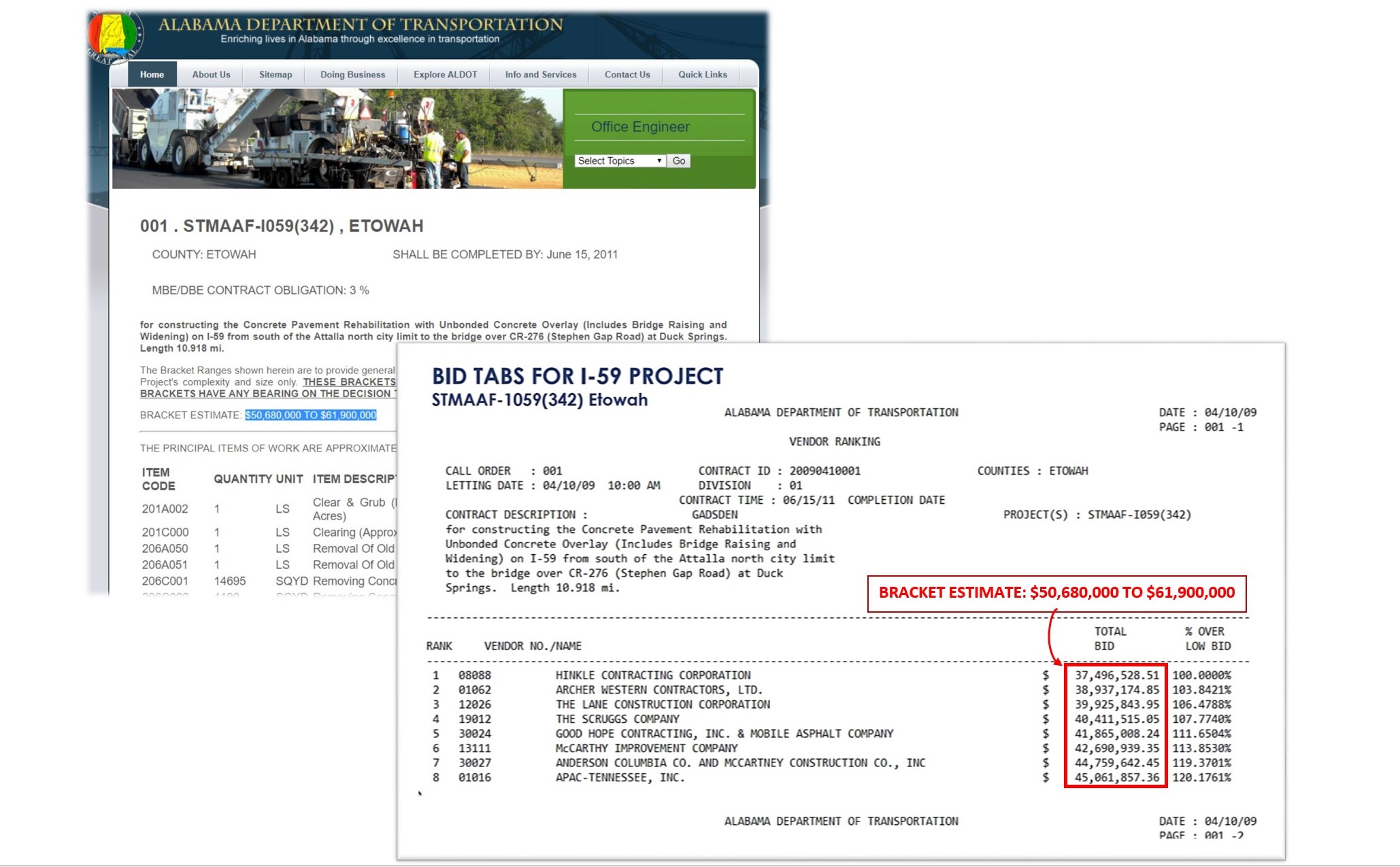

Finally, the April 10, 2009 bids for an I-59 Concrete Overlay Project display how with 8 bidders competing for the contract, all vendor bids come in below the lowest end of the Bracket Estimate.

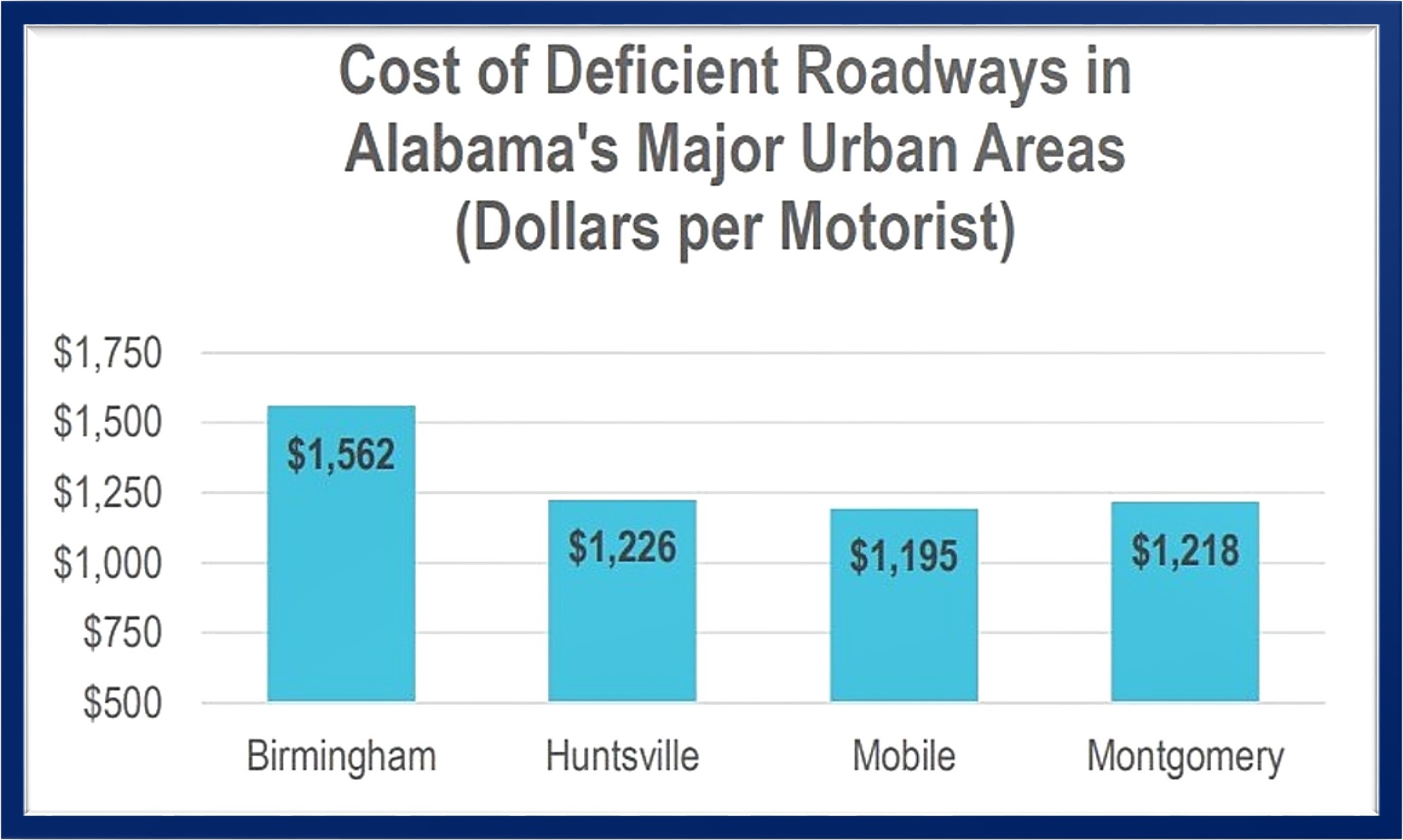

THE ALABAMA SITUATION

Alabama Lacks Competition

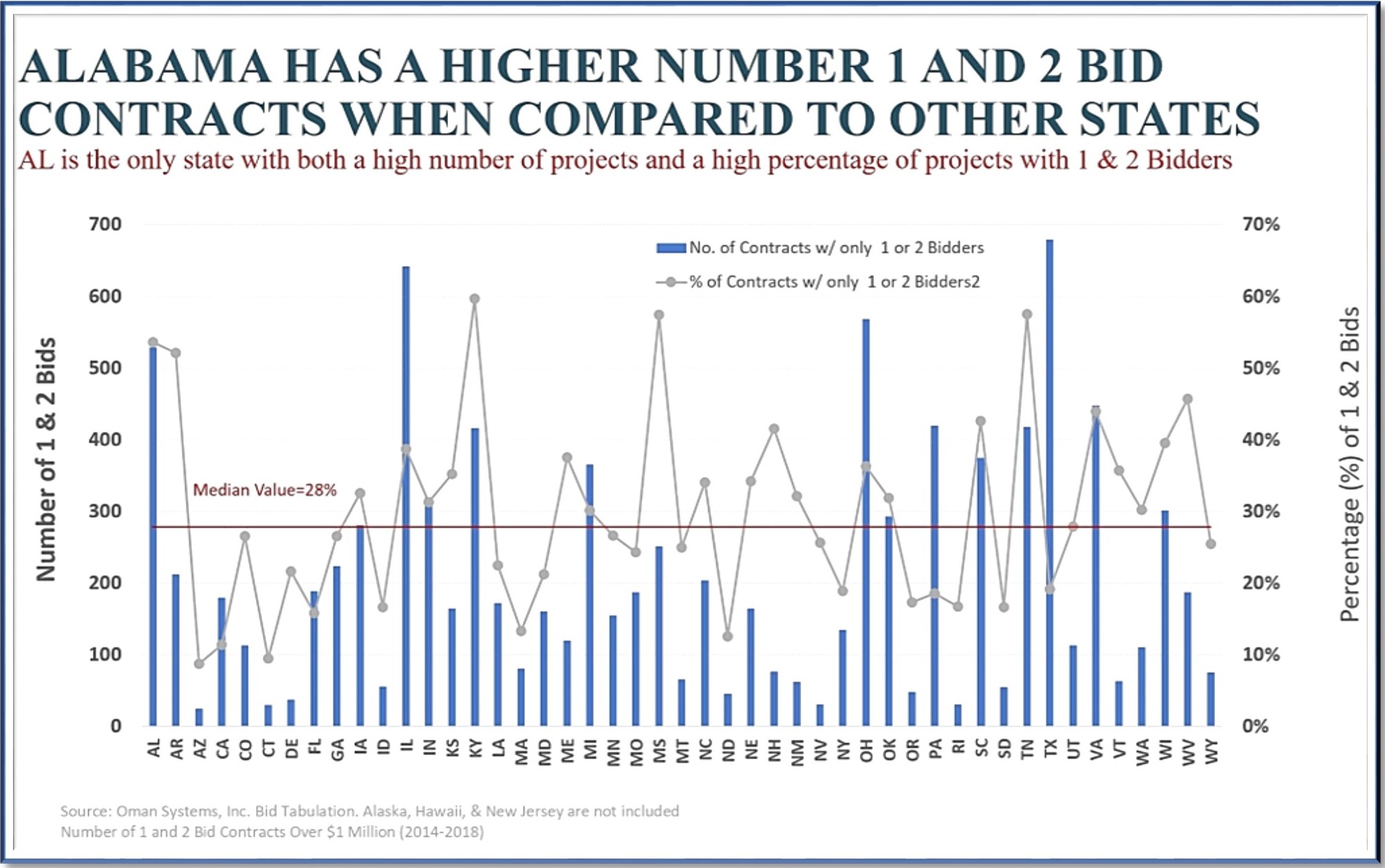

Alabama comes in number 4 in the nation for the highest number of 1 or 2 bid contracts in DOT letting.

This systemic lack of competition has led to contracts awarded above bid bracket estimates, and stagnation.

. . .

2019 ALDOT Letting

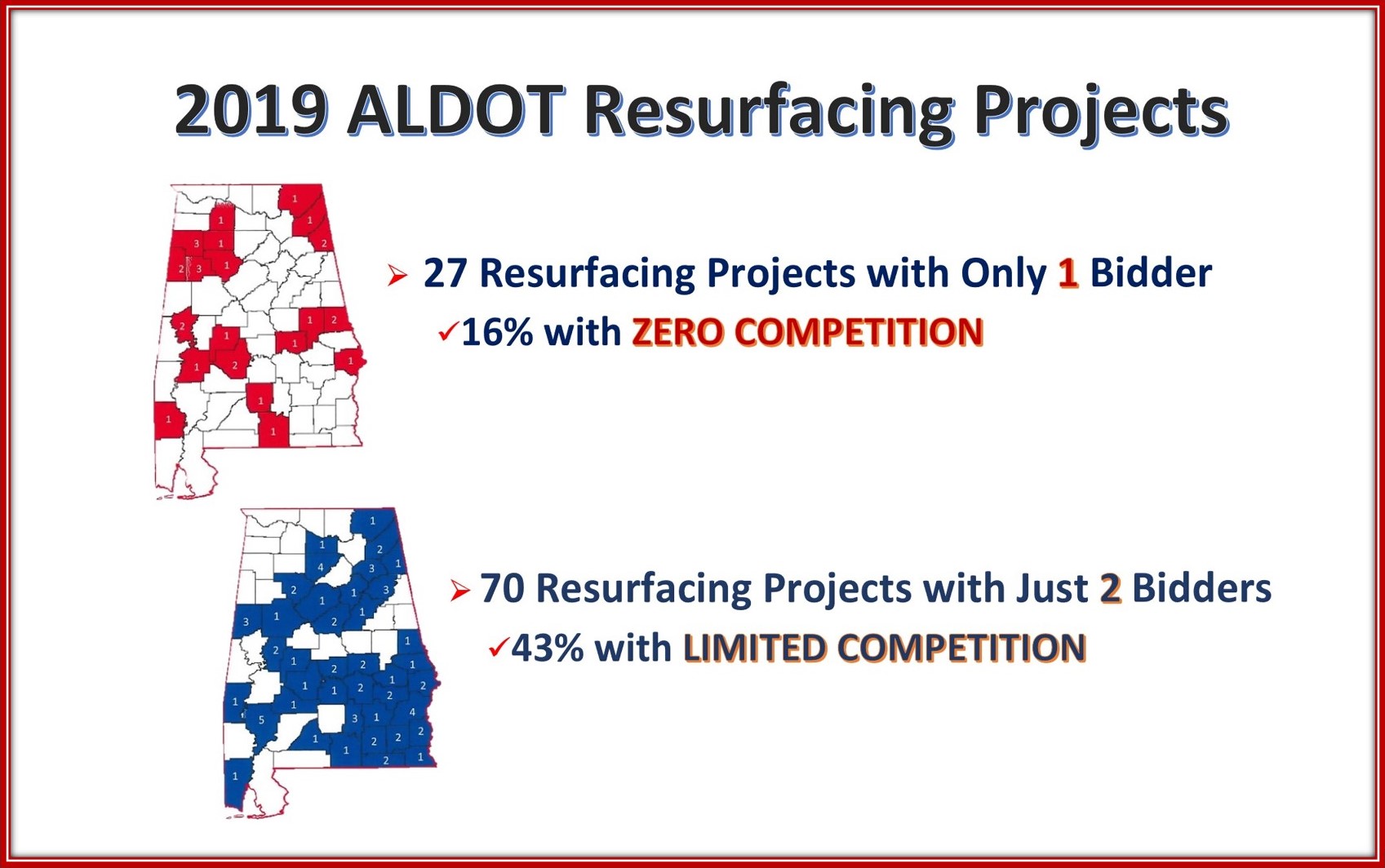

Many areas of the state have LIMITED or ZERO competition on bids.

2019 ALDOT Lettings show that of 162 total resurfacing projects, 97 projects (59%) had only 1 or 2 bidders.

. . .

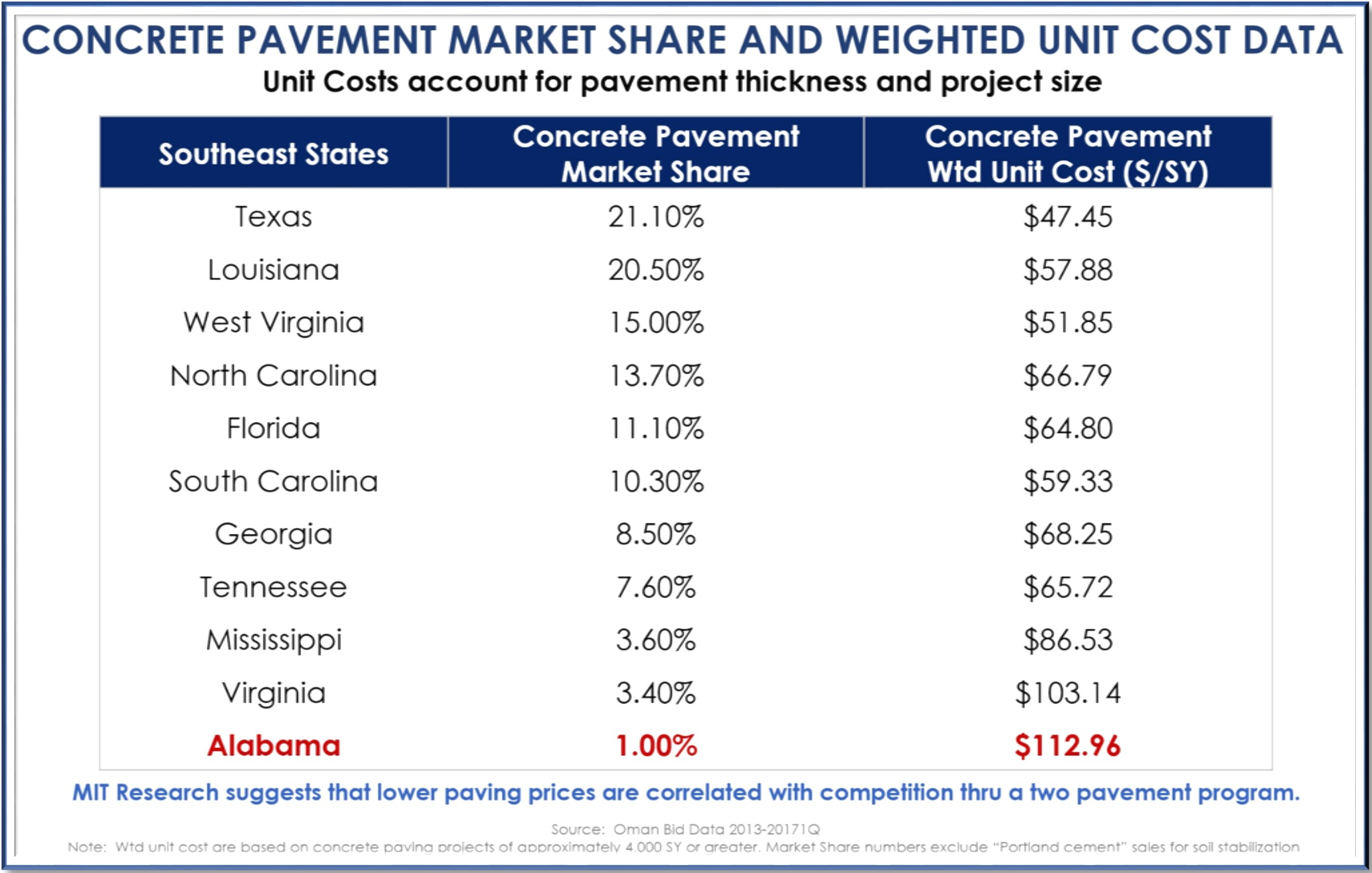

Alabama Pays Most

Of the southeast states, Alabama offers the lowest market share of concrete pavement projects per year.

The result is Alabama paying the highest unit cost for this durable material.

BENEFITS OF INTER-INDUSTRY COMPETITION

Reduced Project Costs

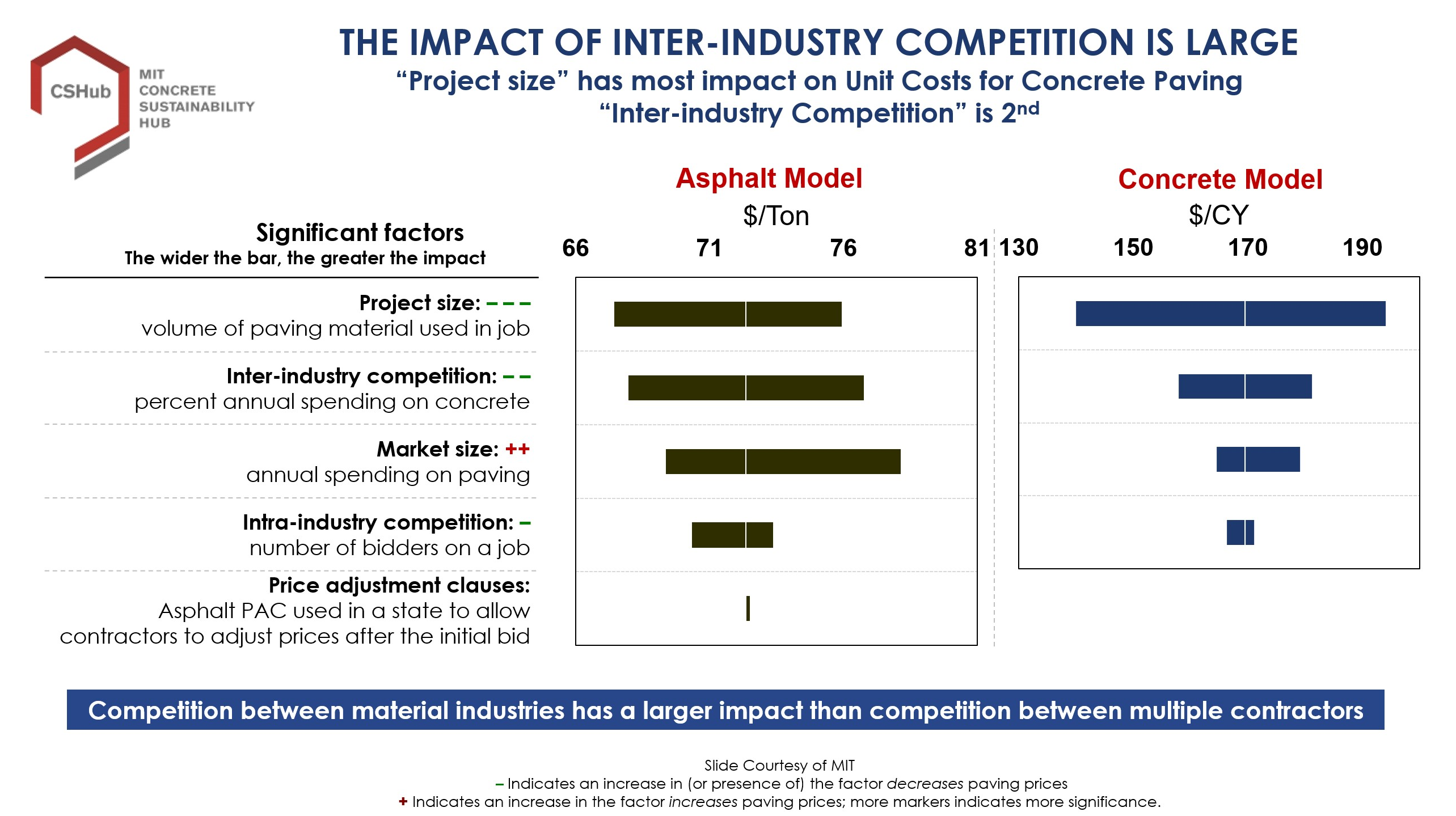

Recently completed research by the MIT Concrete Sustainability Hub shows that states with highest level of industry competition pay ~ 8% and 29% less for asphalt and concrete pavements respectively vs. states with the lowest level of competition.

This happens because industry competition brings additional contractors, and another level of competition to the supply chain that does not occur where only one pavement material is used regularly or exclusively. The result is that states can stretch their scarce transportation funding and touch more roadways.

Enhanced Infrastructure

Now more than ever, given significant economic restraints, growing infrastructure needs, highly uncertain future, and increased public scrutiny, Transportation Agencies need to find effective methods to maximize performance of pavement segments and make their limited infrastructure dollars go farther.

Inter-industry competition (competition between firms that pave with material substitutes) provides this opportunity, leading to an enhanced state infrastructure without increased cost.

Sustained Innovation

In an environment where effectively only one industry participates (i.e. one industry essentially guaranteed to win project bids), the system is much more vulnerable to innovation stagnation and quality challenges (as there is little incentive to invest in either).

Over the last the 25 years, the concrete pavement industry has developed new process, such as Next Generation Diamond Grinding Surface (see photo), and products such as concrete overlays to extend the life of our highway systems.